Employee share schemes

Employee share schemes are a great HR tool, helping companies to hire and retain talent. As the business grows, they incentivise key employees to stay with the business as it grows rather than move on to a new opportunity.

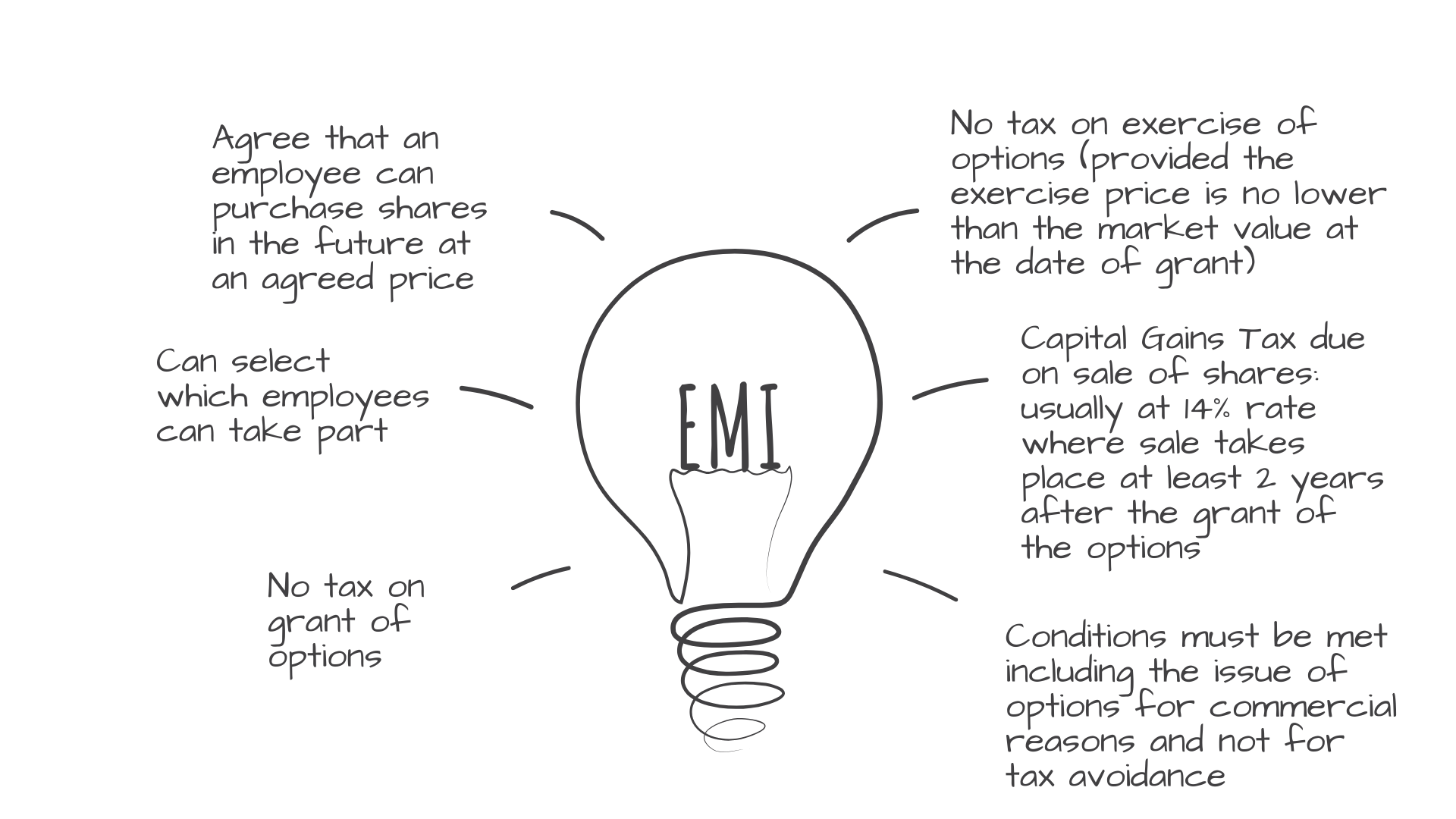

The EMI Scheme

Such schemes also help to ensure that everyone’s priorities are aligned. Research shows that increased productivity and motivation are driven by letting employees have a direct share in the business’s success. In addition, it also enables businesses to incentivise their people without having to pay bonuses. This works well when cash flow is under pressure.

Here, we detail the most popular employee share scheme, the Enterprise Management Incentives (EMI) scheme.

Click image to enlarge …

FAQs

EMI is an HMRC-approved method for giving employees shares in the business in a tax-efficient way. With this scheme, the employee is initially granted something known as an ‘option’. This is basically a right to buy shares at an agreed price in the future.

The two main benefits of EMI schemes are that employees normally don’t have to pay tax when they exercise their option. (i.e. convert it into actual shares). They then pay Capital Gains Tax (“CGT”) rather than Income Tax when they sell their shares. This means that the tax they pay on selling their shares can be as low as 10%, compared to 45% Income Tax. Selected individuals can be invited to take part: the scheme does not have to include all employees.

Without a share scheme, employees who receive shares can incur a hefty Income Tax bill. That is, if they pay less than the market value of those shares. An EMI scheme is an HMRC-approved method for giving employees shares in the business in a tax-efficient way.

A share option agreement is signed by the employee and the company. There is no tax at this stage. This agreement gives an employee the right to purchase shares at an agreed price at an agreed point in future. Provided the agreed price is not lower than the market value at the date the options are issued, no tax is levied when the option is ‘exercised’, i.e. converted into shares.

What are the risks?

This means the option agreement is ‘risk free’ for the employee. If the shares increase in value, they can buy the shares at the lower agreed price. If the value falls, they do not need to exercise the option.

The value of the shares can be agreed with HMRC in advance, although this is not compulsory. Where the value is agreed in advance, this provides the employee with certainty regarding their tax position.

For example:

An employee is given the option to purchase 500 shares for £20 each in three years’ time.

The shares are valued at £20 each at the time the options are granted.

Three years later, the shares are worth £50 but the employee can purchase them for £20 each, with no tax levied on the £30 discount they have received.

The £20 valuation can be agreed in advance with HMRC. This provides certainty for the employee, although this is not mandatory.

When the shares are sold, the gain is taxable under the Capital Gains Tax rules. This is usually at 10% when Business Asset Disposal Relief is available.

Should we give the employee share options or shares?

In many instances, an employee is given share options because this incentivises strong performance. The criteria used for the options to become exercisable (i.e. converted into actual shares) can be chosen by the company. For example, the options might become exercisable after three years, or on achievement of certain performance targets. The only specified rule is that they must be exercisable within ten years. Realistically, in order for an option to act as an incentive, most individuals would expect to be able to exercise it within ten years. So this is not usually a problem.

To be able to issue EMI options:

The company cannot be under the control of another company. Where this is the case, options are often granted in the parent company.

The company can only have ‘qualifying subsidiaries’, of which it owns at least 51%. This can present a problem with 50:50 joint ventures. Subsidiaries that manage property must be 90% owned;

The company must have gross assets of less than £30m;

It must have fewer than 250 employees;

It must undertake a qualifying trade (certain trades, including property development and running hotels or nursing homes, are excluded); and

The company must have a permanent establishment in the UK.

Advance assurance that the company qualifies can be obtained from HMRC. We can draft the application for you. Advance Assurance is not compulsory but can be helpful for Due Diligence proceedings if the company is sold in the future.

Employees (including directors) must work for the company for at least 25 hours per week or, if less, at least 75% of their working time.

Individuals cannot own more than 30% of the shares in the company.

There is an overriding ‘commercial purpose test’ which states that the option must be issued for commercial reasons to recruit or retain an employee, and not for the avoidance of tax.

Employees can have a maximum of £250,000 worth of options and the company can issue a total of £3m in options.

The scheme itself and the options issued under it must be notified to HMRC online by 6th July following the end of the tax year in which the options were granted.

To pass a special resolution, which is needed to make certain changes (such as renaming, restructuring or winding up the company), 75% of shareholder votes are needed. As such, most company owners prefer not to give more than 25% of the shares to other people. The shares given under an EMI scheme can be non-voting shares, but this may be commercially unfeasible, as employees are less likely to pay for shares if these do not enable them to have a vote in decisions affecting the company.

If the options do not become exercisable until the company is sold, this is less of an issue as the control is not given up until the point of sale.

EMI shares must be ordinary share capital, not redeemable or preference shares.

EMI shares can have the right to dividends, but this is not compulsory. No dividends are payable on options, so this is only a consideration once the options are exercised, and shares are granted. If the options are only exercisable on the sale of the business, this will not be a consideration at all.

Most share-option agreements will state that options lapse if an employee leaves. If an employee leaves once they already hold shares, then the situation is more complex and the agreement should be drafted to specify what will happen. Most businesses wish to buy the shares back from the individual at this point, and the share option agreement can specify the price at which this takes place.

No. EMI is meant for small private companies.

If an individual is dismissed for gross misconduct, they would be deemed a ‘bad leaver’. The option agreement would specify what happens to their options and shares if this occurs, but usually, the options would be forfeited, and any shares which have been issued would be repurchased.

The information above does not constitute formal tax advice, and is for general guidance only. Formal advice should be taken before entering into an EMI scheme.

To set up a free call to discuss whether an EMI scheme might help you recruit and retain good people, get in touch via our enquiry form.

This is best illustrated by an example:

Adam is granted a non-tax-advantaged option to purchase shares. Giving him a 5% holding in the company that employs him for £10,000 in three years’ time.

When he exercises the option, the shares are worth £150,000. Adam has to pay Income Tax of up to £67,500 (depending on his personal rate of Income Tax). He has received no cash with which to pay this tax bill.

Two years later, Adam sells the shares for £200,000. He has to pay Capital Gains Tax on the £50,000 increase in value since he acquired the shares. This could be as much as £14,000. Adam’s total tax bill is therefore £67,500+£14,000 = £81,500

At the same time, Eve is granted an EMI option to purchase shares. Giving her a 5% holding in the company that employs her for £10,000 in three years’ time.

When she exercises the option, the shares are worth £150,000. Eve has no Income Tax to pay at this stage.

Two years later, Eve sells the shares for £200,000. She has to pay Capital Gains Tax on the £190,000 increase in value since she acquired the shares: assuming Business Asset Disposal Relief is available, this will be at a rate of 14%, meaning that Eve has a tax bill of £26,600.

Eve’s tax bill is therefore £54,900 lower, because she has been part of an EMI scheme.

It is important to note that one of the conditions set by HMRC for EMI is that the options must be issued for commercial reasons to recruit or retain an employee, and not for the purpose of tax avoidance.

There are other employee share schemes available to companies that don’t qualify for EMI. These include the Company Share Option Scheme (CSOP), growth shares, so-called unapproved/ non tax advantaged share options, Phantom share schemes, Share Incentive Plans (“SIPs”) and Save As You Earn (“SAYE”).

For further details on any of these alternative options, please do not hesitate to contact us.

For EMI options issued after 6 April 2026 onwards, the qualifying thresholds increased. Companies are able to have up to 500 employees (increased from 250), and the gross assets limit will rose to £120 million (from £30m). The maximum value of share options a company can grant was also doubled from £3 million to £6 million. In addition, the time allowed to exercise EMI options is extended to 15 years, and this change also applies to existing EMI options that are still active and haven’t yet been exercised or expired.

Get in touch

To find out how we can help with your requirements, please send a free enquiry.